Indexed Universal Life Insurance: Upside Potential and Downside Protection

Most people know that life insurance provides a death benefit when you die.

But permanent life insurance also offers the potential to grow the value of your policy, as well as downside protection. With indexed universal life insurance, the potential cash value growth is based, in part on the performance of a market index (e.g., the S&P® 500).

All National Life Group indexed universal life insurance products offer a zero percent floor — the least interest you are ever credited is 0%.1

If you need death benefit protection and are interested in growing the cash value of your policy without market risk, indexed universal life insurance may be worth considering.

Key things to know about the upside potential and downside protection offered by indexed universal life insurance:

- The potential growth of the cash value of an indexed universal life insurance policy is based on the performance of a market index like the S&P 500 2 or on a fixed interest rate.

- You typically have a choice of multiple crediting strategies.

- Indexed universal life insurance policies aren't directly invested in a market index.

- Caps and participation rates are important factors in determining how much interest is credited when the market goes up.

- Indexed universal life insurance offers protection and a zero percent floor when the market goes down.

What is the upside potential of indexed universal life insurance?

The potential growth of an indexed universal life insurance policy is based on the performance of a market index in a given period (usually over a one- or two-year period).

A well-known example of a market index is the S&P 500, which includes a representative sample of 500 leading companies in leading industries of the U.S. economy.

Indexed universal life insurance typically offers a choice of interest crediting strategies based on different market indexes, including some that are designed to reduce volatility.3

Which index strategy should I choose?

That is up to you! No one can predict how the market will perform — and just because a strategy performed a certain way in the past, doesn’t mean it will perform that way in the future. You can also pick more than one strategy. However, remember that diversification does not assure a better return.

What if I am worried about having just an annual crediting anniversary?

You have the option to spread your premiums over 12 months, using the Systematic Allocation Rider.

Spreading out your premium over a 12-month period helps capitalize on more potential interest rate crediting dates and reduces risk associated with one annual crediting anniversary. However, this does not guarantee better outcomes.

Until allocated into a monthly crediting strategy, premiums will earn interest in a fixed interest crediting account.

Can I change strategies?

Yes, you can change index strategies at any time. Your new strategies will take effect at the start of the next crediting period. You can change your allocations using the National Life Group customer portal or via our app.

DOWNLOAD THE CUSTOMER APP

Will my policy value grow as much as when I invest directly in the stock market?

Not necessarily. How much interest you are credited depends not just on the performance of the market index, but also on the participation rate and whether there is a cap.

What is a cap?

The cap determines the maximum interest you can earn in a period. For example, if the index grows by 10% but your cap is 6%, your policy will be credited with 6% interest.

Not all index strategies are capped.

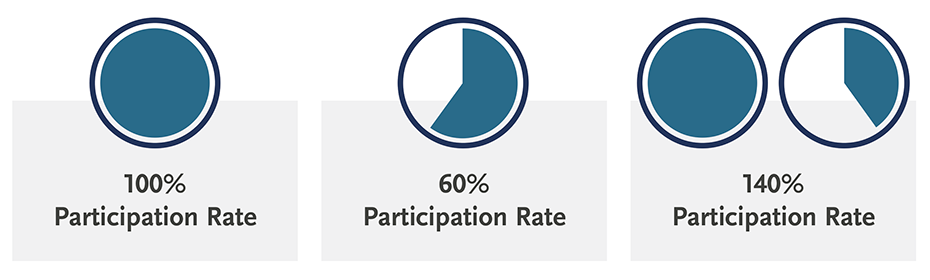

What is the participation rate?

The participation rate determines how much of the market index gains are credited to your policy.

Here are examples illustrating how interest is credited for a specific time period (known as “point to point”), which can be one or two years:

- If the market index gained 8.00% and the participation rate is 140%, you would get credited 11.20% if there is no cap.

- If the market index gained 8.00% and the participation rate is 60%, you would get credited 4.80% if there is no cap.

- The participation rate can also be 100%. In that case, you would get credited at the same rate as the market index gain if there is no cap.

What is the downside protection of indexed universal life insurance?

Sometimes markets go down and an index may lose value in a given period. If you were invested in a index linked security, you would lose money during a downturn.

That’s not true for indexed universal life insurance from National Life Group. When a market index goes down, you are protected from loss. All our indexed universal life insurance products offer a zero percent floor — the least interest you are ever credited is 0%.

Next steps?

- View the differences between interest crediting options and historical performance.

- Learn about volatility-controlled indexes.

- Find out what is best for you and your unique situation: Work with your agent or a financial/tax professional.

1 An Indexed Universal Life (IUL) insurance policy is usually a fixed universal life (UL) policy whose interest is determined, at least in part, by the performance of a specified index of the market. Unlike traditional UL policies, the policy owner may receive zero interest for a single crediting period if the index performs poorly. However, with most designs, the premiums are protected and guaranteed to credit a minimum interest rate in the event the policy is surrendered. The owner of an IUL policy may experience better interest crediting than a traditional UL policy during periods when the market performs well. IUL policies do not directly participate in any stock or equity investments. The amount of interest credited is limited by a “cap”. The 0% or 1% floor provided by an IUL policy ensures that during crediting periods where the index is negative, that no less than 0% or 1% interest is credited to the index strategy. However, monthly deductions continue to be taken from the account value, including a monthly policy fee, monthly expense charge, cost of insurance charge, and applicable rider charges, regardless of interest crediting.

2 The "S&P 500" is a product of S&P Dow Jones Indices LLC or its affiliates ("SPDJI") and S&P Opco, LLC and has been licensed for use by National Life Insurance Company (“NLIC”) and Life Insurance Company of the Southwest ("LSW"). Standard & Poor's® and S&P® are registered trademarks of Standard & Poor's Financial Services LLC ("S&P") and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (''Dow Jones"). The trademarks have been licensed to SPDJI and have been sublicensed for use for certain purposes by NLIC and LSW. The Flexible Premium Adjustable Benefit Life Insurance Policy with Index-Linked Interest Option Policy (“the Policy”) is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, any of their respective affiliates (collectively, "S&P Dow Jones Indices"). Neither S&P Dow Jones Indices nor S&P Opco, LLC make any representation or warranty, express or implied, to the owners of the Policy or any member of the public regarding the advisability of investing in securities generally or in the Policy particularly or the ability of the S&P 500 to track general market performance. S&P Dow Jones Indices and S&P Opco, LLC’s only relationship to NLIC and LSW with respect to the S&P 500 is the licensing of the Index and certain trademarks, service marks and/or trade names of S&P Dow Jones Indices and/or its licensors. The S&P 500 is determined, composed and calculated by S&P Dow Jones Indices or S&P Opco, LLC without regard to NLIC and LSW or the Policy. S&P Dow Jones Indices and S&P Opco, LLC have no obligation to take the needs of NLIC and LSW or the owners of Policy into consideration in determining, composing or calculating the S&P 500. Neither S&P Dow Jones Indices nor S&P Opco, LLC are responsible for and have not participated in the determination of the prices, and amount of Policy or the timing of the issuance or sale of the Policy or in the determination or calculation of the equation by which the Policy is to be converted into cash, surrendered or redeemed, as the case may be. S&P Dow Jones Indices and S&P Opco, LLC have no obligation or liability in connection with the administration, marketing or trading of the Policy. There is no assurance that investment products based on the S&P 500 will accurately track index performance or provide positive investment returns. S&P Dow Jones Indices LLC is not an investment advisor. Inclusion of a security within an index is not a recommendation by S&P Dow Jones Indices to buy, sell, or hold such security, nor is it considered to be investment advice. NEITHER S&P DOW JONES INDICES NOR S&P OPCO, LLC GUARANTEES THE ADEQUACY, ACCURACY, TIMELINESS AND/OR THE COMPLETENESS OF THE S&P 500 OR ANY DATA RELATED THERETO OR ANY COMMUNICATION, INCLUDING BUT NOT LIMITED TO, ORAL OR WRITTEN COMMUNICATION (INCLUDING ELECTRONIC COMMUNICATIONS) WITH RESPECT THERETO. S&P DOW JONES INDICES AND S&P OPCO, LLC SHALL NOT BE SUBJECT TO ANY DAMAGES OR LIABILITY FOR ANY ERRORS, OMISSIONS, OR DELAYS THEREIN. S&P DOW JONES INDICES AND S&P OPCO, LLC MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES, OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE OR AS TO RESULTS TO BE OBTAINED BY NLIC OR LSW, OWNERS OF THE POLICY, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE S&P 500 OR WITH RESPECT TO ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT WHATSOEVER SHALL S&P DOW JONES INDICES OR S&P OPCO, LLC BE LIABLE FOR ANY INDIRECT, SPECIAL, INCIDENTAL, PUNITIVE, OR CONSEQUENTIAL DAMAGES INCLUDING BUT NOT LIMITED TO, LOSS OF PROFITS, TRADING LOSSES, LOST TIME OR GOODWILL, EVEN IF THEY HAVE BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES, WHETHER IN CONTRACT, TORT, STRICT LIABILITY, OR OTHERWISE. THERE ARE NO THIRD PARTY BENEFICIARIES OF ANY AGREEMENTS OR ARRANGEMENTS BETWEEN S&P DOW JONES INDICES AND NLIC OR LSW, OTHER THAN THE LICENSORS OF S&P DOW JONES INDICES.

3 There is no guarantee that index objectives will be met. An Index with volatility control may experience positive Index value change less than that of similar indices that do not include volatility control. This may result in less interest that will be credited. When included in a fixed indexed life insurance policy with the protection of a 0% or 1% floor, the benefit of reduced downside will not be realized for index returns below 0% or 1%.

TC7772562(1225)3